Bitcoin currently underperforms precious metals, with gold reaching a record high while BTC remains range-bound. However, this divergence between Bitcoin and precious metals has occurred before every major cryptocurrency breakthrough since 2019. Declining real yields have driven simultaneous rises in gold and copper prices, with markets pricing in easy liquidity before the Federal Reserve officially cuts rates. Historically, Bitcoin reacts more slowly, but once liquidity signals stabilize, its gains tend to be more pronounced.

Precious Metals Lead Rally Indicates Early Liquidity Shift Signals

(Source: TradingEconomics)

Despite the Fed signaling patience on rate cuts, gold and copper prices are rising. This divergence suggests that markets tend to price in liquidity conditions ahead of official policy shifts, rather than waiting for central bank confirmation. The price movements of these metals are influenced by actual yields, financing conditions, and future expectations—phenomena that are often observed early in easing cycles.

Financial markets tend to reprice before policymakers acknowledge changing conditions, especially when marginal costs of capital begin to shift. The performance of gold across multiple economic cycles clearly confirms this. Data from the London Bullion Market Association (LBMA) and the World Gold Council show that gold prices often start rising months before the first rate cut, as investors react to peaks in real yields rather than rate cuts themselves.

In 2001, 2007, and 2019, gold prices increased even while policies remained “officially” tightening, reflecting expectations that real returns on cash would soon diminish. This leading indicator makes precious metals reliable early signals of changing liquidity environments. The current market pattern feels familiar: as real yields on cash and government bonds decline, gold attracts safe-haven flows.

Copper’s price trend further reinforces this signal because it is driven by different incentives. Unlike gold, copper demand is closely tied to construction, manufacturing, and investment cycles, making it highly sensitive to credit supply and financing conditions. When copper and gold prices rise together, it indicates not only a defensive stance but also market expectations that a loose financial environment will support real economic activity. Recent trends in copper futures on CME and LME show rising prices despite uneven economic data and cautious central banks, indicating a broader perception of liquidity easing.

Triple Implications of Gold and Copper Price Rises

Liquidity Expectation Shift: Markets believe real yields have peaked and are about to decline

Early Cycle Signal: Safe-haven (gold) and growth expectations (copper) rising together signal the start of a loosening cycle

Reduced Misjudgment Risk: A single metal may be affected by geopolitical or supply disruptions, but simultaneous rises reflect systemic liquidity changes

This combination has a significant impact on markets because it reduces the risk of false signals. Gold alone rising might be driven by panic or geopolitical tensions, while copper alone rising could be due to supply disruptions. When both move in tandem, it generally indicates a broader adjustment in liquidity expectations—even if no explicit policy change has occurred, markets are willing to price it in.

Real Yields Are the True Cycle Driver

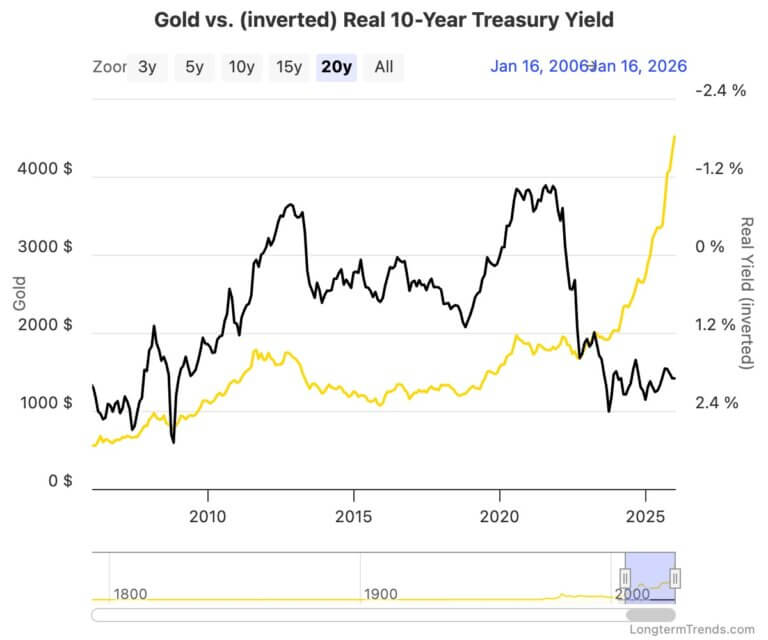

(Source: LongTermTrends)

Gold, copper, and ultimately Bitcoin share a common driver: the real yields on long-term government bonds, especially the US 10-year TIPS yield. Real yields represent the actual return after inflation and are the opportunity cost of holding assets with low or no yields. When these yields peak and begin to decline—even if policy rates remain high—the relative attractiveness of scarce assets increases.

US Treasury data show that gold prices have historically been closely correlated with real yields, often rising after real yields decline rather than after rate cuts. Once real bond yields start narrowing, hawkish rhetoric has rarely reversed this relationship. While copper’s correlation with metals is less direct, it is still influenced by the same background factors: declining real yields tend to coincide with easing financial conditions, a weaker dollar, and improved credit channels—all supporting industrial demand expectations.

The core of the divergence between Bitcoin and precious metals lies in their reaction lag to changes in real yields. Bitcoin follows the same framework but reacts more slowly because its investor base tends to respond only when liquidity signals become clearer. In 2019, Bitcoin’s rally coincided with persistent declines in real yields and accelerated after the Fed shifted from tightening to easing. In 2020, with real yields plunging and liquidity flooding markets, this relationship became more extreme, with Bitcoin’s performance only accelerating after gold re-adjusted.

Capital Rotation Sequence Explains Bitcoin’s Delayed Response

During easing cycles, the order in which assets respond reflects how different types of capital are reallocated. Early in the cycle, investors favor safe, low-volatility assets, supporting demand for gold. As expectations for credit easing and economic growth improve, copper prices begin to rise, reflecting this shift. Bitcoin typically absorbs more capital only after markets gain confidence in easing policies and liquidity conditions can sustain riskier, more reactive assets.

This pattern recurs across cycles. In 2019, gold’s rise preceded Bitcoin’s breakout, with Bitcoin outperforming after rate cuts materialized. In 2020, the timing was shorter but similar: Bitcoin’s largest gains occurred after policy and liquidity measures were already in place. This sequencing explains why Bitcoin may appear disconnected from markets early in cycles. It does not react to isolated data or single rate decisions but to the cumulative effects of shrinking real yields and liquidity expectations, which are often reflected in metals markets early on.

Given Bitcoin’s smaller market size, shorter development history, and sensitivity to marginal shifts, once the position shifts favoring Bitcoin, its price tends to move more violently. Currently, precious metals seem to be re-pricing before the actual trend, while Bitcoin remains range-bound. This divergence often occurs early in easing cycles and only dissipates once real yields continue to decline enough to broadly alter capital allocation.

What Conditions Could Nullify the Divergence and Trigger a Parabolic Rise?

This framework relies on real yields continuing to decline. A sustained rise in real yields would weaken the rationale for gold’s rise, reduce copper’s upward momentum, and also diminish the liquidity support that has historically underpinned Bitcoin’s gains in previous cycles. Accelerated quantitative tightening or a sharp dollar rally would tighten financial conditions and pressure assets that depend on easing expectations.

A resurgence in inflation forcing central banks to delay easing would pose similar risks, as it would push real yields higher and limit liquidity expansion. Markets can anticipate policy shifts, but if economic data contradicts expectations, these expectations cannot be maintained indefinitely.

Factors That Could Nullify the Divergence and Trigger a Parabolic Rise in Bitcoin

Reversal of Real Yields: If inflation is poorly controlled or the economy overheats, real yields could rise again

Accelerated Quantitative Tightening: Faster balance sheet reduction by central banks would tighten liquidity

Significant Dollar Appreciation: A strong dollar typically suppresses all alternative assets, including Bitcoin and metals

Major Delay in Easing: If inflation surges again and rate cut expectations are dashed, market confidence could be undermined

Currently, futures markets are still digesting expectations of eventual easing, and US Treasury real yields remain below cycle highs. Precious metals are reacting to these signals. Bitcoin has yet to show a corresponding response, but historical patterns suggest it often only reacts once liquidity signals stabilize further. If real yields continue to decline, the current metal trends often foreshadow similar or stronger moves in Bitcoin later.

Metal prices are signaling early warnings about financial conditions, even before policy statements acknowledge them. This leading indicator is at the core of the divergence between Bitcoin and precious metals. Once policy catches up with market expectations, Bitcoin—being a high-beta asset—could outperform metals significantly. For investors understanding this cycle, the current divergence is not a sell signal but a potential last opportunity to establish positions.