In mid-January, open interest in Bitcoin options reached $74.1 billion, surpassing futures for the first time at $65.22 billion, marking a shift from directional leverage to structured exposure in the market. Institutions hedge and layer income through options, while retail traders still rely on futures leverage. ETF options are changing market rhythms, with US stock trading hours leaning toward equity markets, while non-trading hours maintain the native crypto characteristics.

Bitcoin options open interest surpasses futures for the first time

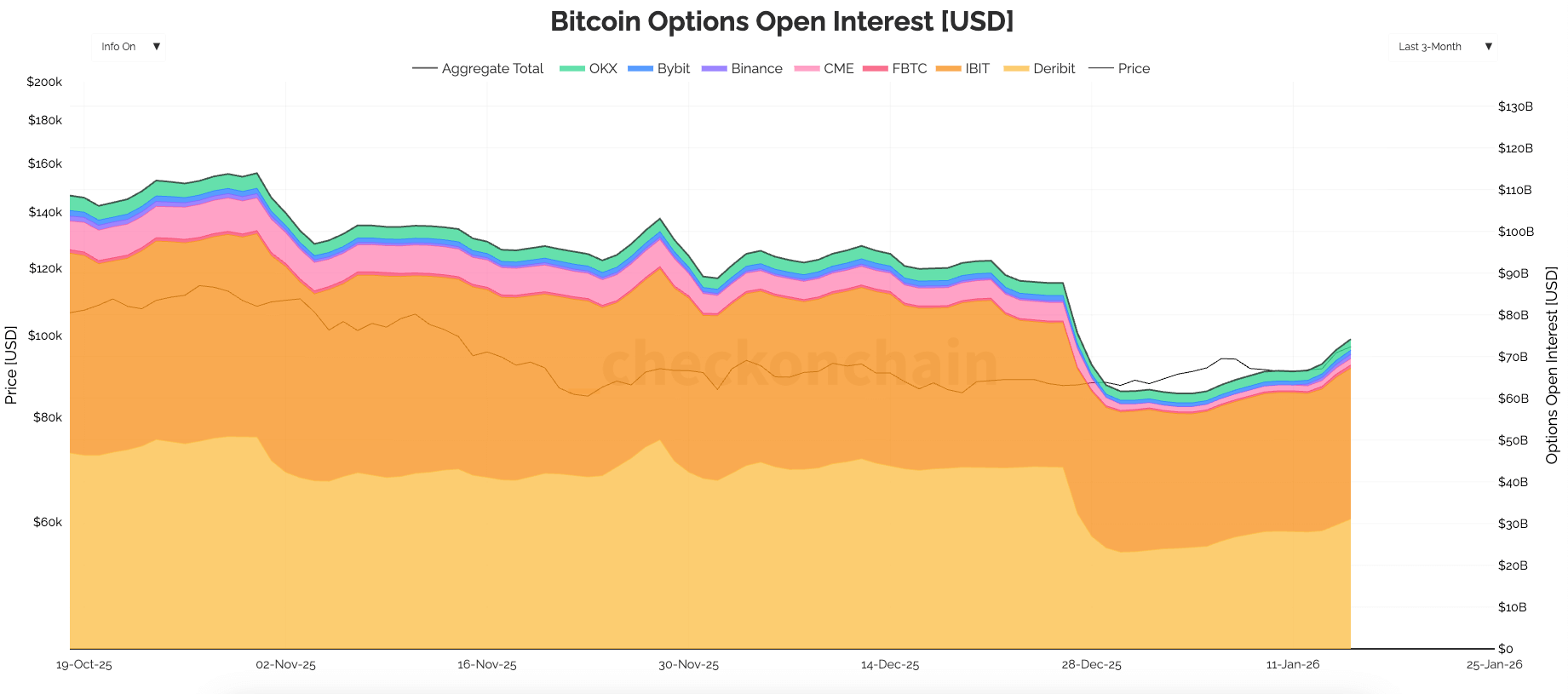

(Source: Checkonchain)

By mid-January, the open interest in Bitcoin options increased to approximately $74.1 billion, slightly exceeding the open interest in Bitcoin futures at around $65.22 billion. Open interest refers to the total number of unsettled or expiring contracts, thus measuring position holdings rather than trading activity. When options open interest exceeds futures, it generally indicates the market relies less on pure directional leverage and more on structured exposure: hedging, income layering, and volatility positions.

Futures remain the simplest way to participate in Bitcoin price movements with leverage. However, Bitcoin options allow traders and institutions to more precisely control risk through income strategies, limit losses, profit from price increases, or trade specific volatility outcomes. This distinction is crucial because options positions tend to be held longer than futures positions, and this persistence influences key strike prices, expiration dates, and volatility near liquidity windows.

The fact that options trading volume surpasses futures is a significant milestone, impacting daily Bitcoin trading substantially. Futures trading aims for direct exposure and quick repositioning, with traders posting margin, buying or selling contracts linked to Bitcoin, and managing funding rates, basis changes, and increasing liquidation risks as leverage multiplies. Futures positions can expand rapidly but are highly sensitive to holding costs.

The different performance of options stems from their typical use as long-term investment tools rather than mere leverage. Calls and puts convert expectations into explicit income structures, while spread options, calendar options, and covered calls transform spot risk exposure into manageable risk positions. This results in positions that can last weeks or even months, often linked to hedging, systematic income plans, or rolling volatility strategies.

Core differences between options and futures

Holding period: Options can last weeks to months; futures are usually short-term with frequent adjustments

Risk profile: Options have limited losses and unlimited gains; futures carry two-way unlimited risk

Purpose of use: Options mainly for hedging and income; futures primarily for directional leverage

Clearing pressure: Options have no clearing risk; futures with high leverage are prone to forced liquidation

Institutional hedging strategies dominate market structure shifts

As options open interest grows, market makers’ roles become increasingly important. Dealers acting as intermediaries in Bitcoin options trading typically hedge using spot and futures, influencing price movements near strike prices and expiration dates. In markets with concentrated positions, hedging can suppress or accelerate volatility depending on the distribution of risk exposure across strike prices and maturities.

High open interest in options can also serve as an indicator of rising hedge intensity, especially when liquidity thins or market congestion increases. Checkonchain data shows that options open interest plummeted sharply in late December and then rebounded in early January, consistent with a pattern of risk re-establishment after major contract expirations to prepare for the next cycle.

Meanwhile, Bitcoin futures open interest appears more stable and has increased more significantly, reflecting that futures positions are continuously adjusted rather than mechanically liquidated at expiration like options. This difference explains why, even amid volatile prices and uncertain market confidence, options can surpass futures.

What has changed is the entities holding options risk and their motivations. An increasing share of options risk reflects layered portfolio allocations and structured capital flows rather than pure speculation. This helps explain why, even during periods of deleveraging driven by futures market financing, basis compression, and hedging sentiment, open interest in options remains high.

ETF options and native crypto markets diverge further

Bitcoin options are no longer a single unified ecosystem. Checkonchain’s exchange options data shows that, besides common crypto trading platforms, a growing segment related to listed ETF options—such as IBIT—is emerging. This segmentation is crucial because it alters trading rhythms, risk management mechanisms, and demand-driving strategies.

Native crypto options trading platforms operate in a continuously trading environment, including weekends, using cryptocurrencies as collateral, serving proprietary trading firms, crypto funds, and mature retail clients. Listed ETF options trade during US market hours, employing clearing and settlement structures familiar to equity options traders.

As a result, a larger proportion of volatility risk can be reflected within regulated onshore mechanisms, even though global Bitcoin trading remains 24/7. Market trading hours alone can reshape or even dominate market behavior. When a significant portion of options trading concentrates during US hours, hedging activity becomes more synchronized during these times, while offshore venues often lead price discovery during non-trading hours and weekends.

Clearing and margin discipline also influence participation. Listed options use standardized margin and centralized clearing, with many institutions prepared to utilize these structures, expanding participation to firms unable to bear risk on offshore exchanges. These participants bring mature trading strategies, including covered call strategies, calendar spreads, and volatility targeting.

Retail leverage space squeezed by institutional hedging strategies

When options open interest exceeds futures, short-term market behavior is more susceptible to position structure and hedging liquidity. Excessive futures leverage often triggers rapid declines in open interest through capital feedback loops, basis dislocations, and cascade liquidations, making retail leverage operations highly vulnerable.

Options-dense markets typically express pressure through expiration cycles, strike price concentration, and dealer hedging, which can suppress or amplify spot price volatility depending on the distribution of risk exposure. Macroeconomic news and spot market dynamics remain important, but market direction may hinge on the distribution of options risk and how dealers hedge.

The key point is that derivatives positions have become a more significant driver of short-term price movements. Monitoring options open interest across different venues helps distinguish offshore volatility positions from onshore ETF-linked hedging strategies, while futures open interest remains a key indicator of leverage and basis preferences. The same total amount can imply very different risk conditions.

As ETF options liquidity grows and native crypto trading venues continue to dominate continuous trading, Bitcoin’s volatility may increasingly reflect the interaction between US market liquidity and 24/7 crypto liquidity. This crossover points to a market where positions, expirations, and hedging mechanisms play larger roles in price trends, while retail participation through simple futures leverage is being squeezed.