The Ministry of Finance’s clarification explicitly states that gains from cryptocurrency trading are classified as property transaction income. The National Taxation Bureau has already identified underreporting of NT$129 million and imposed penalties, bringing virtual assets fully into the taxation and regulatory system.

As virtual assets like Bitcoin gradually become part of the public investment portfolio, whether gains from cryptocurrency trading are taxed has become a focus of regulatory and tax policy discussions. Ernst & Young (EY) pointed out that according to the latest Ministry of Finance interpretation, profits from buying and selling cryptocurrencies can now be recognized under the current Income Tax Act as “property transaction income,” subject to taxation.

The National Taxation Bureau has identified NT$129 million in unreported cryptocurrency trading income

According to a written report submitted by the Ministry of Finance to the Legislative Yuan, the National Taxation Bureau has made cryptocurrency trading a key focus of audits. As of mid-December 2024, tax authorities have identified approximately NT$129 million in underreported income, with additional taxes and penalties totaling about NT$34.03 million.

In a report by the Commercial Times, EY Tax Services Operations Manager Lin Chih-hsiang stated that cryptocurrencies are virtual digital assets based on blockchain technology. Although they lack physical form and are not issued by central banks, the economic benefits generated from their trading should still be recognized under current tax regulations. For profit-seeking enterprises and high-net-worth individuals, failure to properly understand reporting timing or rules could result in back taxes or penalties.

EY: Cryptocurrency trading in Taiwan is now within the scope of taxation

EY pointed out that, according to the Ministry of Finance’s letter No. 11304672340, profits from trading cryptocurrencies can be taxed as property transaction income under the Income Tax Act. EY further analyzed that Taiwan has not yet established a dedicated cryptocurrency tax system; existing regulations are mainly supplemented by interpretive notices. However, under the current system, related trading gains are substantively included in the scope of taxation, and tax authorities are continuously enhancing their ability to gather and verify data on virtual assets, including comparing exchange data and fund flows.

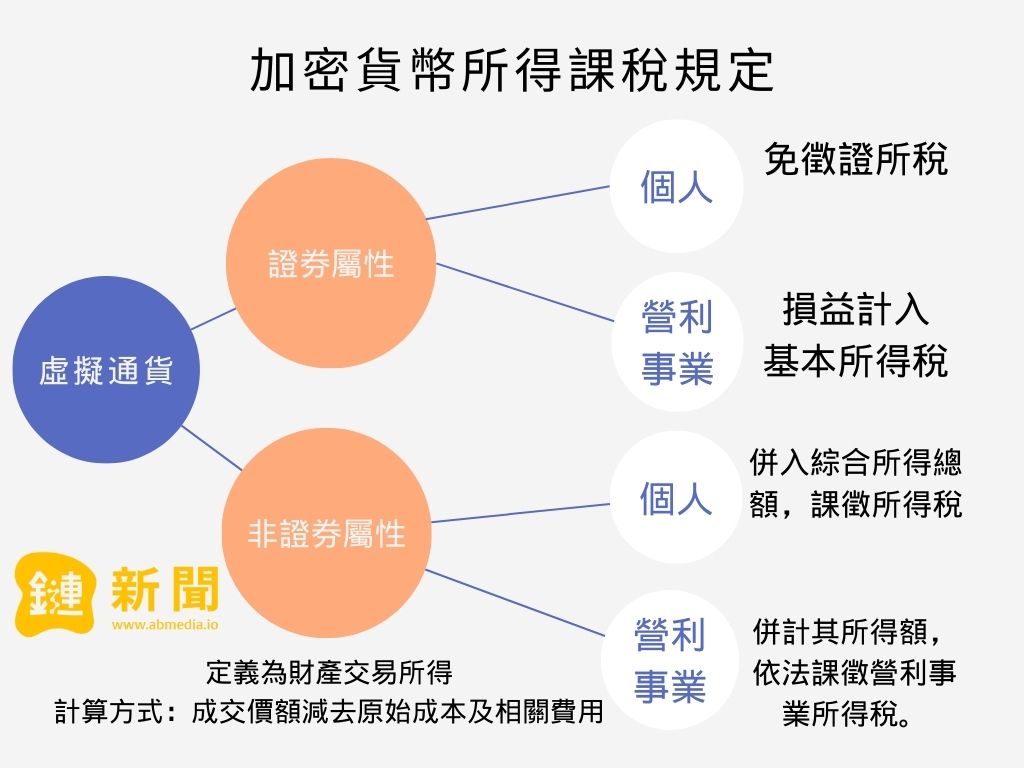

According to a previous report by Chain News, the Ministry of Finance has considered regulations for taxing cryptocurrency income. Profits from buying and selling virtual currencies of a securities nature are classified as “securities trading gains and losses.” For virtual currencies that are not securities, the transaction price minus costs is included in individual comprehensive income tax, while profits for profit-seeking enterprises are combined with their income and taxed as corporate income tax. Key issues include what constitutes non-securities trading and the criteria for determining whether a virtual currency has securities characteristics, which warrant further attention.

Source: Chain News

- This article is reprinted with permission from Chain News

- Original title: “Will Cryptocurrency Trading in Taiwan Be Taxed in 2026? EY: According to the Income Tax Act, Considered Property Transaction Income”

- Original author: Neo

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.